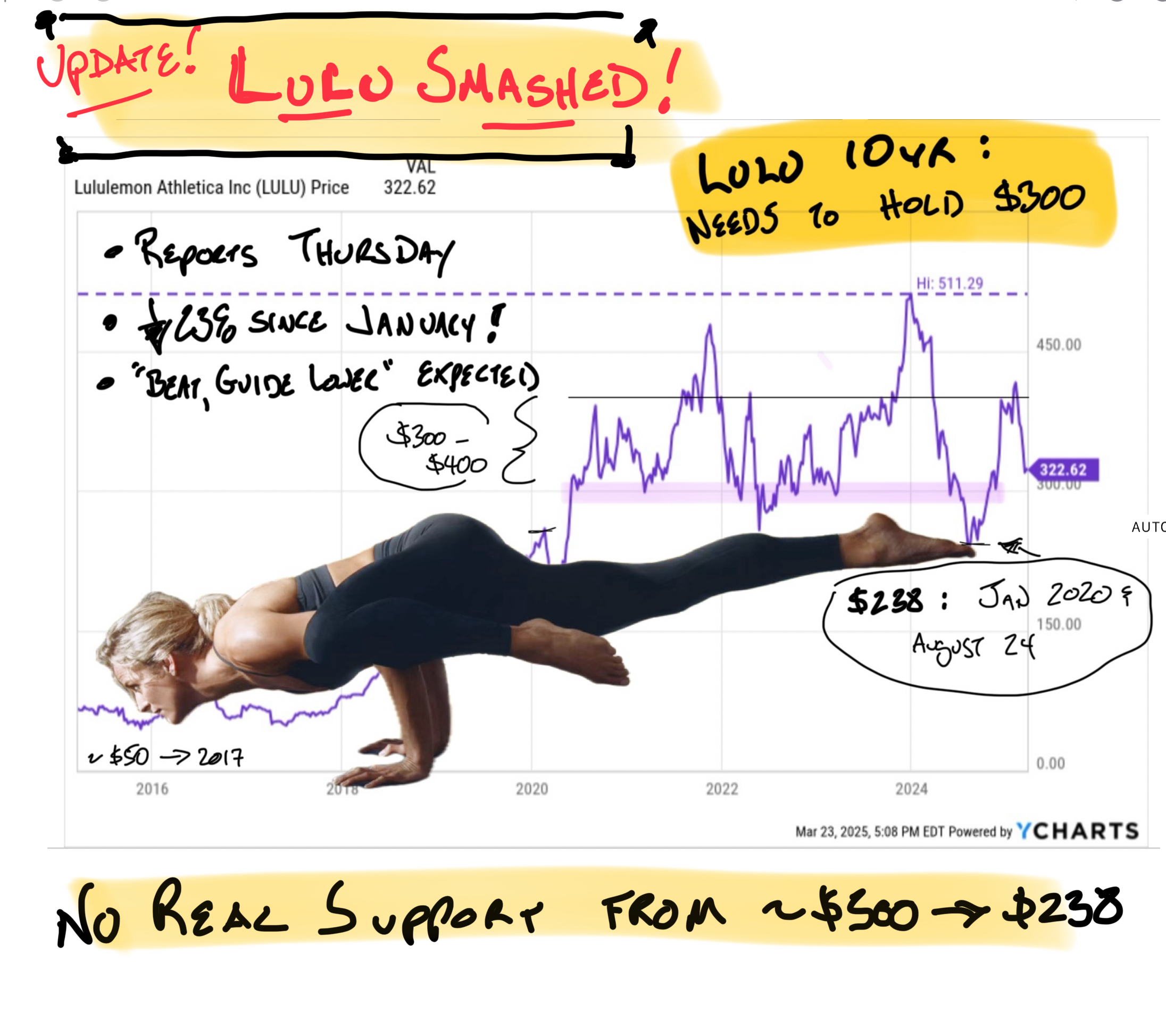

Lululemon is getting boot-stomped early Friday after the company.... wait for it... beat earnings estimates and guided lower than Wall Street's official estimate for the first quarter and all of 2025.

There are a few reasons investors shouldn't have been shocked by LULU's soft guide. "Beat and Guide Lower" has been the theme of retail earnings for over a month, as featured in this article called "Beat and Guide Lower' is 2025's Hottest Trend". Lulu flagged weakness in North America a year ago, way before it was hip and the stock has been a murder-pit ever since. Which is also not a secret and something I discussed earlier this week.

Lulu is who we thought they were but that's not proving to be a good enough reason for buyers to step in as the stock probes the bottom of a multi-year range in between $300 and $400 (save for a few spikes):

A few thoughts:

LULU's Growth Problem Is Real

Since 2021 LULU has grown revenues at a CAGR of 19%, expanded margins 170bps and increased EPS from ~$4.50p/s to over $14p/s. In 10yrs Lulu grew its men's business from a couple hundred million to over $2b/yr. Athleisure for Men has gone from a joke to just "clothing"; a victory for men who like comfort and me, personally, as someone who spent a decent portion of my life 10 years Evangelizing for men as a frustrated Lulu shareholder.

Really. Here I am in 2016, talking with my friend Andy Swan about Lululemon's opportunity to dominate men's pants with my friend Andy Swan.

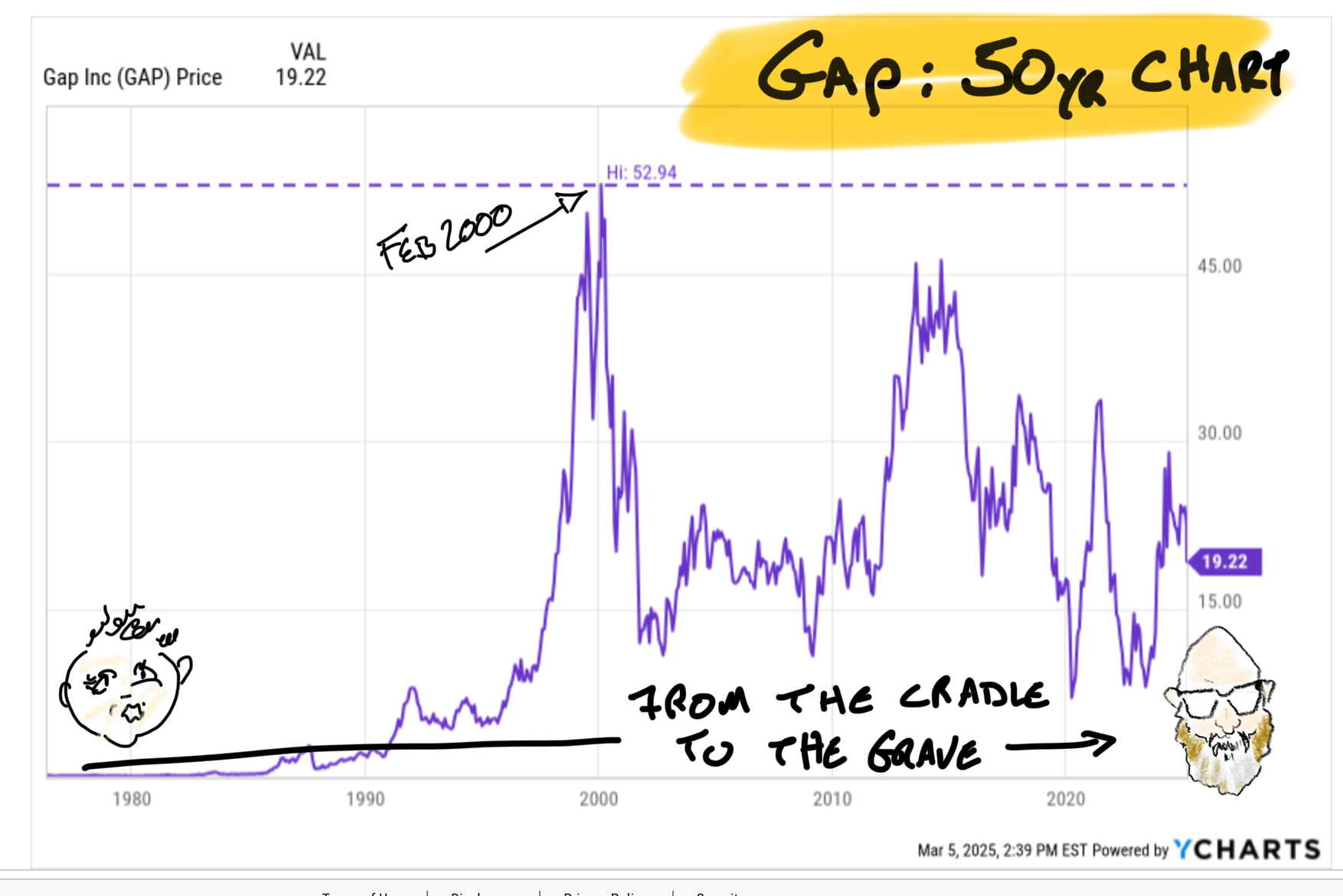

Lulu was $55 in 2016 and hit $500 in late 2013. The company created the modern retail model where e-commerce is a core element of the business, right from the start. While Gap was trying to strap e-commerce to the back of an overgrown store base Lululemon from tracking inventory with chips, making the app an indispensable and seamless part of the shopping experience. It's been a GD glorious run and I thank every vest-wearing Millennian banker in Anti-Ball-Crushing pants:

Alas, the glory days are gone and it's not looking transitory. Lulu has grown revs over 19% since 2021 but just guided to 5% topline expansion this year after scraping out a double-digit gain last year. Margins remain an industry wonder but analysts accept as gospel the idea that flat revenue growth will lead to margin compression.

You're left with a slowing (at best), post-peak margin company. Lulu prints cash and is buying back shares but they don't have much of a specific plan about how to keep growing from here. There's an argument to be made that Lulu shouldn't try to keep from becoming even more mainstream than it already is but philosophical debate isn't going to move Lulu's P/E back to 35x next year's earnings.

Lulu won the war. History hasn't been kind to retailers in this position, as long-term Gap investors know:

You can play the trading range, look for a bounce or try to grind out a little more on the short side of Lulu. I've got some thoughts on just that in the + space. But those are trades. It's going to be a few years before the company becomes a Buy and Hold name again.

Specialty is where love goes to die. It's healthier and more profitable to focus more on the journey.

You need to have a subscription to access this content in full.